IC Autodesign owner

Why Welders Are in High Demand in Sweden

Sweden is currently experiencing a strong and sustained demand for skilled welders, driven by a combination of structural labor shortages and large-scale industrial transformation. This demand is not temporary—it is tied to long-term national priorities such as decarbonization, industrial expansion, and infrastructure renewal.

1. The Green Transition Is Reshaping Industry

One of the biggest forces behind the rising demand is Sweden’s aggressive shift toward a low-carbon economy. Major investments in renewable energy and sustainable infrastructure are creating continuous demand for skilled metalworkers.

Welders are essential in building and maintaining:

Wind turbines and offshore wind platforms

Hydropower plants and energy systems

New green technology facilities and industrial equipment

These projects often require advanced welding certifications and strict adherence to environmental and safety standards, raising the overall skill requirements and value of experienced workers.

2. Industrial Expansion in Northern Sweden

Northern Sweden has become a focal point for some of Europe’s largest industrial development projects. Massive investments in green steel production, battery manufacturing, and energy-intensive industries have created an unprecedented need for construction and fabrication workers.

These developments are not small-scale—they involve entire industrial ecosystems, including:

Large-scale factory construction

Heavy steel structures and pipelines

Continuous maintenance and expansion work

As a result, thousands of new welding positions have emerged in regions that previously had limited industrial employment opportunities.

3. An Aging Skilled Workforce

A major structural challenge is the aging population of skilled tradespeople. Many experienced welders are approaching retirement, and the pipeline of younger workers entering the profession has not been sufficient to replace them.

This creates a dual pressure:

Loss of experienced mentors and technical knowledge

Immediate labor shortages in critical industries

Training programs exist, but the gap between retiring professionals and new entrants continues to widen, keeping demand high.

4. Infrastructure, Manufacturing, and Shipbuilding Needs

Beyond new green projects, Sweden’s traditional industrial base remains strong and continuously requires welding expertise.

Key areas include:

Railway construction and maintenance

Heavy industrial fabrication and repair

Automotive manufacturing supply chains

Shipbuilding and marine engineering

These sectors rely on welding not only for new production but also for ongoing maintenance and structural repairs, ensuring stable long-term demand.

Beyond Retirement: How Organizations Are Preserving Critical System Knowledge for the Next Generation

Across industries, organizations are facing a transformation that receives far less attention than cloud migration or AI adoption, yet may prove just as consequential: the retirement of the experts who built and maintained their most critical business systems.

For decades, core enterprise applications have been supported by highly experienced developers and architects whose knowledge extends far beyond programming languages or technical documentation. They understand how systems behave under pressure, why certain business rules exist, and how decades of operational decisions shaped today’s application landscape. In many organizations, that knowledge exists primarily in the minds of a small number of individuals now approaching retirement.

The systems they support, however, are not disappearing. Adabas & Natural applications continue to power essential operations across banking, insurance, government, manufacturing, and other industries. These platforms process millions of transactions every day while supporting business processes that evolve continuously alongside changing customer expectations and regulatory demands.

For organizations planning for the future, the challenge is no longer simply maintaining legacy systems. It is ensuring that the business knowledge embedded within those systems can be understood, supported, and extended by a new generation of developers—without introducing operational risk or overwhelming already stretched IT teams.

The Growing Risk of Knowledge Concentration

Many organizations eventually recognize the same pattern: critical expertise has become concentrated among a handful of long-serving employees.

These individuals often possess years of accumulated operational understanding that never made its way into formal documentation. They know which integrations are sensitive, which workflows contain hidden dependencies, and which business processes evolved through years of practical adaptation. Their expertise comes from experience rather than manuals.

At the same time, organizations are being asked to do more with fewer resources. Workloads continue to increase while internal IT teams remain under pressure to maintain daily operations, support modernization efforts, and respond quickly to business demands. As a result, there is rarely enough time available for structured mentoring, training, or knowledge transfer.

When this imbalance persists, organizations begin experiencing cascading operational risks. Development projects slow because fewer people understand application dependencies. Enhancements become harder to implement safely. Teams grow increasingly cautious around critical systems because confidence diminishes when only one or two people fully understand how applications behave.

Over time, even routine maintenance can become difficult.

Why Traditional Hiring Alone Isn’t Enough

Most organizations respond to generational change by trying to expand staffing before senior experts depart. Companies hire junior developers, increase contractor support, and invest in mainframe or Natural training programs for existing employees.

These efforts are necessary, but they rarely solve the entire problem.

Internal teams often lack the bandwidth required to mentor new hires while simultaneously managing production workloads. Recruiting experienced mainframe professionals has become increasingly difficult and expensive in a highly competitive talent market. Meanwhile, relying too heavily on individual experts creates dangerous single points of failure that only intensify over time.

Organizations that navigate generational change successfully approach it differently. Rather than treating it as a staffing challenge alone, they view it as a long-term capability and resilience initiative.

The most effective strategies combine people, processes, and technology to distribute knowledge more broadly across teams while building confidence systematically.

Strategies That Help Organizations Succeed

Organizations managing generational transition effectively tend to share several common practices.

Combining Internal and External Expertise

Many companies are supplementing internal teams with external specialists while simultaneously developing in-house capabilities. This approach allows organizations to maintain operational stability while accelerating knowledge transfer.

One Nordic financial services organization paired junior developers with retired experts serving as mentors. Structured training programs helped newer employees absorb both technical and operational knowledge more efficiently while reducing pressure on internal staff.

Replacing Informal Handoffs with Structured Programs

Ad-hoc onboarding processes rarely provide enough consistency for complex enterprise systems. Organizations increasingly rely on formal mentorship programs, rotational learning paths, and try-and-hire models that allow new developers to become familiar with systems before assuming full responsibility.

A Swiss manufacturing company used this approach to attract technology talent despite operating in a remote location. By integrating consultants into long-term mentoring programs, the company successfully transitioned several external specialists into permanent team members.

Modernizing Development Environments

Development tooling also plays a major role in reducing barriers for newer developers.

Modern environments such as NaturalONE and the upcoming Natural for Visual Studio Code help bridge the gap between traditional enterprise systems and contemporary development practices. Familiar interfaces, integrated workflows, and improved collaboration capabilities make it easier for developers to become productive quickly.

A U.S.-based manufacturer improved operational stability after adopting these modernized development tools, enabling experienced developers and newer hires to collaborate more effectively across teams.

Investing in Continuous Learning

Organizations are also expanding training beyond traditional classroom approaches. Virtual learning, hands-on mentoring, guided onboarding, and AI-assisted development tools are helping teams accelerate skill development while preserving operational continuity.

For example, a European insurance company maintained productivity during a platform rehosting initiative by combining structured technical support with long-term training and mentoring programs.

Capturing Institutional Knowledge

Perhaps most importantly, organizations are focusing on reducing reliance on undocumented tribal knowledge. Standardizing processes, documenting workflows, and embedding business logic into development practices all help ensure critical expertise remains accessible after experienced employees retire.

This shift transforms knowledge from an individual asset into an organizational capability.

How Modern Tools Are Changing the Transition Process

Technology is becoming an increasingly important part of managing generational change successfully.

Software AG’s modernization approach combines consulting, training, and development tooling to help organizations preserve knowledge while modernizing operational practices.

NaturalONE, the company’s Eclipse-based development environment, already provides capabilities that improve productivity and collaboration for Natural developers. Natural for Visual Studio Code, scheduled for release in 2026, is designed to make Natural development more familiar and accessible for developers entering enterprise IT environments today.

At the same time, Natural AI Code Assist is expected to further accelerate onboarding and learning by helping developers understand unfamiliar codebases, generate documentation, and reduce the time required to become productive within complex applications.

Together, these tools support a broader modernization strategy focused not only on technology, but also on long-term workforce sustainability.

Turning Generational Change Into an Opportunity

Generational transition does not have to threaten operational stability. In many cases, it can become an opportunity to modernize development practices, improve resilience, and distribute knowledge more effectively across teams.

Organizations that act early are often able to reduce operational risk significantly while making core applications more approachable for the next generation of developers.

The alternative is far riskier. Every retirement without a knowledge transfer plan increases the likelihood that critical operational insight disappears permanently.

As workloads continue growing and experienced experts leave the workforce, organizations must find sustainable ways to bridge past and future. Those that combine modern tooling, structured learning, and proactive succession planning will be best positioned to preserve the value embedded within their applications for years to come.

Sweden is facing a growing shortage of engineers and technical professionals, creating strong opportunities for qualified candidates. With demand expected to exceed supply through 2028, companies across the country are actively seeking skilled talent—both locally and internationally.

Where the Demand Is Highest

Tech & IT

Sweden’s digital economy is expanding rapidly, with a projected shortage of around 18,000 tech professionals each year. Software developers, IT architects, and cybersecurity specialists are especially in demand.

Engineering Roles

There is consistent demand for engineers across multiple disciplines, including mechanical, electrical, chemical, and mining engineering.

Construction & Manufacturing

Companies are also looking for building services engineers and technical specialists to support infrastructure and industrial projects.

Why There’s a Talent Shortage

- Aging workforce – Many experienced professionals are reaching retirement age

- Skills gap – Not enough graduates to meet industry needs

- Location challenges – Fewer candidates are willing to relocate to northern Sweden, where many large projects are based

What This Means for Candidates

- Competitive salaries, especially in IT and specialized engineering

- Strong job prospects across multiple industries

- Opportunities for international candidates, with many employers open to hiring from abroad

What Employers Are Doing

- Hiring internationally to fill critical roles

- Offering higher salaries and benefits to attract talent

- Expanding teams through global and offshore solutions

- Supporting work permits via initiatives like the EU Blue Card

Important to Know

While demand is high, some roles—especially outside international tech companies—require Swedish language skills. However, many global companies operate in English and actively welcome international professionals.

A Changing Threat – An Adaptable Solution

The world beneath the oceans is evolving just as rapidly as the one above. Advances in technology, shifting geopolitical dynamics, and new access routes—particularly in the Arctic—are redefining what is possible below the surface. Capabilities once considered unattainable are now not only feasible but essential. As artificial intelligence accelerates decision-making and autonomous systems expand operational reach, the underwater domain is becoming a critical frontier for both opportunity and risk.

For modern states, safeguarding the future means more than traditional defense. It requires protecting critical national infrastructure, securing vital shipping lanes, and maintaining control over the seabed environment. These demands call for highly capable, flexible, and enduring underwater assets—systems that can operate farther, longer, and with greater adaptability than ever before.

At the forefront of meeting these challenges is Saab, whose approach to submarine and underwater technology is rooted in continuous evolution. Rather than designing platforms that risk becoming obsolete, Saab embraces a modular philosophy—one that allows systems to grow, adapt, and remain relevant as threats and missions evolve.

An Evolutionary Approach to Underwater Superiority

For more than a century, Saab has been a pioneer in submarine innovation. Its legacy includes milestones that have shaped modern naval engineering—from the introduction of fully welded submarine hulls in the 1930s to the development of the X-form rudder in the 1960s. In the decades that followed, Saab helped revolutionize air-independent propulsion, dramatically extending underwater endurance.

Today, Saab continues to lead with fully digitized submarines capable of integrating into complex “system-of-systems” environments. These platforms can seamlessly operate alongside uncrewed underwater vehicles (UUVs), enabling coordinated missions that enhance surveillance, defense, and operational flexibility.

Central to this capability is Saab’s modular design philosophy. Submarines are built with adaptability in mind, allowing for straightforward upgrades and retrofits throughout their lifecycle. This ensures that each vessel can evolve in step with emerging technologies and shifting operational demands—remaining effective not just at launch, but for decades to come.

A Legacy of Innovation Across Generations

Saab’s expertise is reflected in its development of more than 20 submarine classes over the past century. Beginning with early designs in the early 20th century, each generation has introduced new technologies and refined operational capabilities.

From improved hull shapes that enhance hydrodynamics and stealth, to advanced propulsion systems that extend submerged endurance, Saab’s submarines have consistently pushed the boundaries of underwater performance. Innovations such as stealth-enhancing coatings, advanced maneuverability systems, and record-setting weapons capabilities demonstrate a commitment to both technological excellence and operational effectiveness.

Modern Saab submarines continue this tradition, with built-in capacity for mid-life upgrades that keep them at the cutting edge of performance long after deployment.

Meeting Diverse Operational Needs

Saab’s submarine portfolio is designed to address a wide range of naval requirements, divided into two primary segments:

- Oceanic Submarines: These form the backbone of Saab’s offering, combining over a century of expertise with forward-looking design. They are optimized for versatility, stealth, and sustained operations in complex maritime environments.

- Expeditionary Submarines: Built for extended missions and long-distance deployments, these larger platforms support greater crew capacity and increased payloads. They are ideal for navies operating far from home waters, requiring endurance and strategic reach.

Complementing these manned platforms is Saab’s Autonomous Ocean Drone, a large uncrewed underwater vehicle (LUUV). Drawing on Saab’s deep heritage in submarine technology, this system represents the next step in underwater operations—delivering rapid adaptability in an environment where change is constant.

Prepared for an Uncertain Future

As the underwater domain becomes increasingly contested, adaptability is no longer optional—it is essential. Saab’s evolutionary approach ensures that its submarines and underwater systems are not only capable today but ready for tomorrow’s challenges.

In a world where tides shift quickly and threats evolve even faster, the ability to adapt is the ultimate advantage.

By 2026, the automotive industry has entered a new era where software and artificial intelligence shape nearly every aspect of a vehicle. Cars are no longer defined solely by mechanical engineering; instead, they operate as highly connected digital platforms. This shift toward Software-Defined Vehicles (SDVs) allows automakers to manage and upgrade critical vehicle functions—ranging from braking systems to infotainment—through software.

Artificial Intelligence now plays a central role across the entire automotive ecosystem. Beyond powering advanced driver assistance, AI is used to design vehicles, optimize manufacturing processes, and create highly personalized in-car experiences tailored to each driver.

Key Technology Trends

Software-Defined Vehicles (SDVs)

Modern vehicles are increasingly described as “computers on wheels.” In an SDV architecture, most features are controlled by software rather than fixed hardware. This enables manufacturers to deliver large over-the-air (OTA)updates that can enhance performance, add new features, or improve safety without requiring a dealership visit. For example, companies such as Volvo can update millions of vehicles simultaneously through cloud-based systems.

Electrification and Advanced Battery Technology

Solid-State Batteries

Solid-state batteries are widely considered the next major breakthrough for electric vehicles. They promise to double energy density, significantly extend driving range, and reduce charging times to as little as 10–15 minutes. Several manufacturers are already testing prototypes capable of exceeding 1,000 km per charge.

Alternative Powertrains and Efficient Motors

Advances in electric motor design are also improving efficiency. Motors built using innovative materials such as amorphous steel are reaching efficiency levels close to 98%, helping vehicles travel farther while consuming less energy.

Autonomous and Connected Mobility

Level 3 and Level 4 Automation

Autonomous driving technology continues to evolve. Level 3 systems—where the vehicle can handle driving under certain conditions—are becoming more common in production vehicles. Meanwhile, robotaxi fleets operating at Level 4 autonomy are expanding in major cities, providing driverless ride-hailing services.

Vehicle-to-Everything (V2X) Communication

With the rollout of 5G connectivity, vehicles can communicate with surrounding infrastructure, other vehicles, and even pedestrians. This real-time data exchange helps improve traffic flow, prevent collisions, and enhance navigation.

Next-Generation Cabin and Safety Innovations

AI-Driven Personalization

In-car artificial intelligence can now learn driver preferences and habits over time. Vehicles automatically adjust seat positions, cabin temperature, lighting, and entertainment options based on the driver’s profile. Some automakers are also integrating advanced conversational AI assistants to enable natural voice interaction with vehicle systems.

Immersive Displays and Augmented Reality

New display technologies are transforming dashboards. Augmented Reality (AR) head-up displays project navigation guidance directly onto the windshield, aligning digital directions with the real road ahead. Some concept vehicles feature panoramic displays spanning the entire width of the dashboard.

By-Wire Technology

Traditional mechanical connections—such as steering columns—are increasingly replaced with electronic control systems. Steer-by-wire technology eliminates physical steering linkages, allowing more flexible cabin designs and adjustable steering responses tailored to different driving conditions.

Advanced Driver Monitoring Systems

Enhanced safety features now include intelligent monitoring systems that track driver alertness. Cameras and sensors analyze blinking patterns, eye movement, and facial expressions to detect fatigue or distraction. If a potential risk is detected, the vehicle can issue warnings or recommend a break.

Sustainable Manufacturing and Design

Circular and Eco-Friendly Materials

Sustainability is becoming a core design principle. Automakers are introducing bio-based plastics made from sugarcane, recycled fishing nets, and plant-derived leather alternatives for vehicle interiors, reducing environmental impact while maintaining durability.

Digital Twins

Manufacturers are increasingly using digital twin technology—virtual replicas of vehicles and production facilities—to simulate millions of test kilometres. This allows engineers to identify potential issues and optimize manufacturing processes before building physical prototypes.

3D Printing and Lightweight Components

Additive manufacturing enables the production of complex parts that would be difficult to create using traditional methods. These 3D-printed components are often lighter and more efficient, helping reduce vehicle weight and improve overall energy efficiency.

The Automotive Update: EV momentum lifts EU market as Tesla drops models and leans into AI

Europe’s new-car market returned to growth last year, supported by rising demand for electrified powertrains, while the global automotive industry continued to adjust to shifting trade dynamics and strategic realignments. Developments ranged from progress in EU–India trade relations to major production decisions by Tesla and expansion plans from Chinese carmaker Chery.

EVs underpin EU new-car growth in 2025

Europe’s new-car market closed 2025 in positive territory, with registrations across the EU’s 27 member states rising 1.8% year on year. The improvement was driven by six consecutive months of growth at the end of the year.

Data from ACEA shows electrified vehicles continuing to gain ground. Battery-electric vehicles (BEVs) and plug-in hybrids (PHEVs) together accounted for nearly 2.9 million registrations during the year, representing around 27% of the total market.

BEVs alone made up 17.4% of all new-car deliveries. Despite this shift, petrol cars remained a major force, still capturing more than a quarter of total registrations.

Hybrids—combining full and mild-hybrid systems—emerged as the most popular powertrain overall in 2025, topping the rankings for the first time.

At a country level, Spain stood out with double-digit growth in new-car registrations, supported by strong EV demand and incentives. Germany, Europe’s largest market, returned to modest growth, while France and Italy both recorded year-on-year declines.

Uncertainty clouds Spain’s next EV incentive scheme

In December, Spain confirmed that its long-running MOVES programme would be replaced by the new Auto 2030 Plan, also known as PlanAuto+. The scheme is due to launch at the beginning of 2026, but key funding criteria have yet to be published.

This delay has raised concerns about a potential gap in incentives, which could slow the market. Under the new structure, subsidies would be managed centrally rather than by Spain’s autonomous regions. The government has earmarked €400 million for EV purchase incentives in 2026, broadly in line with previous annual MOVES budgets.

However, according to reports from electrive, approval is being held up by the Ministry of Economic Affairs. The intention is to move towards a system similar to France’s, where incentives are linked to a vehicle’s overall CO₂ footprint. While the original plan aimed to favour EU-built EVs without excluding others, eligibility criteria are now expected to become more restrictive.

EU carmakers welcome India trade agreement

European manufacturers have reacted positively to the conclusion of free-trade negotiations between the EU and India. ACEA said the agreement could significantly improve access to a market of around four million annual passenger-car sales, where import tariffs can reach as high as 110%.

While quotas and residual duties will still limit the full impact, the industry expects meaningful benefits once the detailed terms are assessed.

India is also rising in strategic importance for European brands. Renault has identified the country as a key growth market, citing improved access for EU manufacturers following the trade deal.

Tesla cuts models as focus shifts to AI and robotics

Tesla is preparing to discontinue two of its longest-running vehicles as it accelerates investment in artificial intelligence and robotics.

The move follows a challenging set of fourth-quarter results that underlined a difficult year for the carmaker. According to the Financial Times, Tesla plans to end production of the Model S and Model X in the next quarter.

The report also suggests that Tesla’s California facility could be repurposed as a manufacturing hub for its Optimus humanoid robots. In parallel, the company is expected to invest around $2 billion (€1.7 billion) into Elon Musk’s xAI venture.

Chery eyes UK manufacturing base

Chinese manufacturer Chery is exploring the possibility of producing vehicles in the UK, potentially using an existing plant owned by Jaguar Land Rover.

Sources cited by the Financial Times indicate that discussions are under way to use a current manufacturing facility to build Chery’s EVs in Britain. The UK government has reportedly been courting the company for several years.

Chery’s Omoda and Jaecoo brands are among the fastest-growing Chinese marques in the UK, alongside rivals such as BYD. The country has seen a surge of competitively priced Chinese vehicles, partly as manufacturers seek alternatives to EU markets where tariffs on China-built EVs have increased.

Chery has already entered the UK market with the Tiggo 7, Tiggo 8 and Tiggo 9, underlining its longer-term ambitions in Europe.

Germany’s automotive industry is entering what many analysts describe as a “make-or-break” period, as deep structural problems collide with an uncertain economic outlook and an uneven transition to electric mobility. Once the undisputed backbone of Europe’s industrial economy, the sector is now grappling with falling profits, aggressive global competition, and mounting pressure to reinvent itself for an electric, software-driven future.

At the heart of the crisis lies the difficult shift to electric vehicles (EVs). German manufacturers have poured tens of billions of euros into electrification, yet demand has failed to grow as quickly or as sustainably as expected. While EV sales recovered in 2025, much of that rebound reflected a correction after earlier subsidy cuts rather than a genuine surge in consumer appetite. Compared with rivals, German firms continue to lag in software development, charging infrastructure integration, and clear long-term EV strategies.

The financial strain is becoming increasingly visible. Industry heavyweights including Volkswagen, BMW, and Mercedes-Benz have all reported sharp declines in profitability. The situation has been particularly severe at Porsche, where profits plunged by roughly 95 percent, underscoring how even premium brands are struggling to shield themselves from market headwinds.

Competition is intensifying on multiple fronts. Chinese manufacturers are rapidly expanding their market share, both domestically in China and increasingly across global markets, benefiting from scale, lower costs, and strong state backing. At the same time, the prospect of higher U.S. tariffs on imported vehicles adds another layer of uncertainty for German exporters already under pressure.

The pain is spreading through the supply chain. Major suppliers are cutting jobs as they restructure for a future with fewer combustion-engine components. Bosch and ZF alone have announced the elimination of thousands of positions, highlighting the social and economic consequences of the industry’s transformation.

Yet the picture is not uniformly bleak. Recent production data has surprised to the upside. In November 2025, German industrial output rose unexpectedly, driven largely by a jump in car manufacturing. This ended a multi-month streak of declines and offered a rare positive signal in an otherwise fragile environment. Even so, overall vehicle sales remain well below their 2017 peak, reinforcing the sense that the recovery is incomplete.

Looking ahead to 2026, the challenges remain formidable. A true, self-sustaining recovery in the EV market has yet to materialize. Tighter EU emissions regulations will raise compliance costs, while continued advances by Chinese competitors threaten German firms’ traditional strongholds. Domestically, high living costs and elevated electricity prices risk further dampening consumer spending on big-ticket items like cars.

Recent strategic decisions reflect the pressure to adapt. Volkswagen’s decision to close its joint-venture plant in Nanjing with SAIC Motor underscores the difficulties German manufacturers face even in markets that once fueled their growth.

In essence, Germany’s auto industry stands at a crossroads. The sector remains a cornerstone of the national economy, but its future competitiveness will depend on decisive strategic shifts—particularly in electrification, software, and cost structures. Whether 2026 becomes a turning point or a further step in relative decline will hinge on how effectively the industry navigates this historic transition.

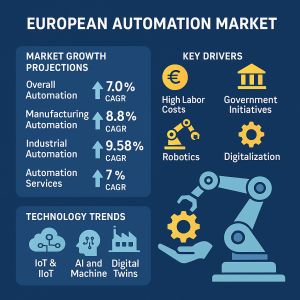

Europe’s Automation Revolution: AI, Robotics, and Digitalization Drive a New Era of Industrial Efficiency

The European automation market is entering a period of unprecedented growth, driven by digital transformation, labor cost pressures, and rapid technological innovation. Across industries—from manufacturing to logistics—automation is reshaping operations, creating smarter, more efficient, and more connected production ecosystems. With the rise of artificial intelligence (AI), industrial IoT (IIoT), and robotics, Europe is positioning itself as a global leader in intelligent automation.

Market Overview and Growth Projections

Automation in Europe is expanding across multiple segments, with compound annual growth rates (CAGR) frequently surpassing 8% in core industrial areas.

Overall Automation: The European automation market is projected to grow at a 7.0% CAGR between 2026 and 2033, potentially reaching $160 billion by 2033.

Manufacturing Automation: Expected to expand at a CAGR of around 8.8%–8.9% through 2031, with Germany remaining the continent’s dominant market.

Industrial Automation: Forecast to grow at 8.5%–9.6% CAGR between 2024 and 2032, supported by the increasing adoption of smart factories and connected systems.

Automation Services: The industrial automation services market is predicted to rise at 7% CAGR through 2030.

Marketing Automation: Strong growth is also observed in marketing automation, driven by Europe’s high digital engagement and the use of AI-based personalization tools.

This broad-based expansion highlights Europe’s strategic commitment to automation as both a productivity enabler and a competitive differentiator in the global economy.

Key Growth Drivers

1. High Labor Costs

With Europe facing some of the world’s highest labor costs, automation has become an essential strategy for maintaining competitiveness. Manufacturers are investing heavily in robotic and digital systems to improve efficiency and reduce dependency on manual labor.

2. Government Initiatives

Public policy is playing a central role. Across the EU, national and regional governments are incentivizing Industry 4.0adoption—supporting modernization through funding, tax credits, and technology programs focused on digital transformation and sustainability.

3. Technological Advancements

Robotics: The surge in robot adoption—particularly collaborative robots (cobots)—is revolutionizing manufacturing flexibility and safety.

Digitalization: A growing emphasis on connected and secure production systems is driving the digital transformation of factories.

IoT and IIoT: The Industrial Internet of Things enables real-time data exchange between machines, increasing visibility and control across production lines.

AI and Machine Learning: These technologies are ushering in self-optimizing, predictive automation, enabling systems to learn, adapt, and improve autonomously.

Digital Twins: Companies increasingly use digital twin models to simulate processes, test configurations, and perform predictive maintenance—reducing downtime and accelerating innovation.

4. Operational Efficiency

Automation investments are primarily driven by the pursuit of efficiency and cost optimization. Intelligent control systems, AI analytics, and integrated platforms allow companies to streamline workflows and maximize output with minimal waste.

5. E-commerce and Logistics

The rise of e-commerce has significantly accelerated warehouse and logistics automation, with robotic picking systems, automated guided vehicles (AGVs), and autonomous mobile robots (AMRs) improving speed and accuracy in order fulfillment.

Major Segments and Emerging Trends

Hardware Leadership

In manufacturing automation, hardware remains the largest revenue-generating segment, driven by demand for robots, controllers, and sensors. Continuous innovation in mechatronics and robotics ensures this category will retain its leadership through 2030 and beyond.

Software Integration

Software is the glue connecting automation ecosystems. Growth in Manufacturing Execution Systems (MES), Enterprise Resource Planning (ERP), and AI-based monitoring tools reflects the increasing need for seamless data integration between operational and business layers.

Warehouse Automation

This segment continues to accelerate, propelled by logistics modernization and rising online retail volumes. Automated sorting, packaging, and transportation systems are becoming standard across Europe’s largest distribution centers.

OT/IT Convergence

The merging of Operational Technology (OT) and Information Technology (IT) is transforming industrial architecture. Unified data environments enable end-to-end visibility—from factory floors to enterprise dashboards—paving the way for smarter, autonomous operations.

Conclusion

Europe’s automation market stands at the crossroads of innovation and necessity. With powerful growth drivers—from AI and robotics to digital twins and IoT—automation is evolving from a competitive advantage into a fundamental business requirement.

As industries across the continent embrace smart manufacturing, connected supply chains, and data-driven operations, Europe’s automation ecosystem is poised to define the global standards for efficiency, sustainability, and intelligent design.

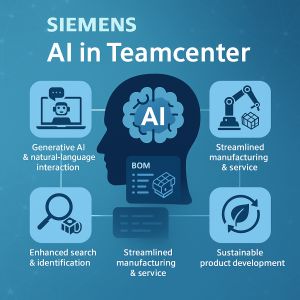

Siemens Digital Industries Software has taken a major step toward intelligent product lifecycle management (PLM) by integrating advanced AI into its Teamcenter platform. The latest Teamcenter 2506 release and the introduction of Teamcenter Copilot bring generative AI, natural-language interaction, and visual intelligence directly into the heart of product development, manufacturing, and service.

Smarter Collaboration with Generative AI

At the center of this update is Teamcenter Copilot, a conversational assistant powered by large language models (LLMs) and securely grounded in a company’s own Teamcenter data.

Conversational Search & BOM Exploration: Users can ask natural-language questions to explore 3D product structures, trace part usage, or filter BOM data.

Document Analysis: The Copilot can summarize large documents, extract requirements, or create tables and bullet lists for faster reviews.

Custom Knowledge Bases: Organizations can build AI knowledge bases tailored to specific products or projects for more relevant responses.

Enhanced Search and Identification

Visual Search: Powered by Azure AI Vision, users can upload a photo to identify similar parts—useful for finding replacements or unknown components.

Natural-Language Search: Instead of complex keyword queries, users can simply ask questions across structured and unstructured Teamcenter data.

These tools make information retrieval faster and more intuitive across teams and disciplines.

Streamlined Manufacturing and Service

AI is also reshaping execution workflows:

AI-Generated Manufacturing Instructions: Upcoming features in Teamcenter Easy Plan will automatically generate and translate work instructions.

Service Planning Automation: AI can create detailed maintenance and service plans by analyzing configurations and past service records, reducing planning time and errors.

Intelligent Data Management and Sustainability

Classification AI: Automatically assigns classes to files, reducing manual effort by up to 90%, while experts validate results through human-in-the-loop review.

AI-Powered Lifecycle Assessment (LCA): Teams can evaluate environmental impact and compliance across a product’s lifecycle—supporting sustainability goals.

Built on Secure, Flexible Architecture

All AI features use a Retrieval-Augmented Generation (RAG) architecture, ensuring answers are based on verified internal data. The platform runs flexibly on major cloud providers like Microsoft Azure or on-premises, protecting IP while enabling scalability.

The Bigger Picture

By embedding AI across its PLM ecosystem, Siemens is transforming Teamcenter from a data repository into an intelligent partner that drives speed, accuracy, and innovation. Engineers, planners, and service teams can now interact naturally with their data, automate repetitive tasks, and make faster, better-informed decisions—paving the way for a new era of digital engineering.

In modern industrial facilities, piping networks are the lifelines that transport fluids, gases, and steam essential for operations. But behind every well-functioning piping system is an often-overlooked discipline: pipe stress analysis. Stress analysis tools aren’t just about checking boxes—they’re essential for ensuring safety, reliability, and long-term cost efficiency.

Preventing Catastrophic Failures

A single piping failure can shut down an entire facility. For example, in 2012, Chevron’s Richmond refinery in California suffered a catastrophic pipe rupture due to corrosion and inadequate stress management. The incident caused massive fires, exposed thousands of people to harmful chemicals, and cost Chevron over $2 billion in settlements and upgrades. Proper stress analysis could have flagged vulnerabilities in the piping system long before failure.

Stress analysis software like CAESAR II or AutoPIPE simulates real-world operating conditions—pressure, vibration, thermal expansion, and seismic loads—to identify risks early. By doing so, companies avoid disasters that threaten human lives, the environment, and corporate reputation.

Ensuring Regulatory Compliance

Regulatory codes such as ASME B31.3 (Process Piping) and ASME B31.1 (Power Piping) mandate stress analysis. Skipping it isn’t just unsafe—it’s illegal. For example, Fluor Corporation, one of the largest engineering and construction firms, integrates stress analysis into all its oil & gas and power projects to guarantee code compliance. This prevents costly redesigns, failed inspections, and project delays.

Accommodating Thermal Expansion

In industries like power generation, steam lines can reach extreme temperatures. General Electric (GE), when designing piping systems for its steam turbines, uses stress analysis to account for expansion and contraction that occurs with temperature swings. Expansion loops, bellows, and flexible joints are engineered into the design to prevent buckling or cracking. Without this, pipes could literally tear themselves apart during operation.

Optimizing Pipe Support Design

Improperly supported piping can sag, vibrate excessively, or overload connections. ExxonMobil, in its petrochemical plants, relies on advanced stress analysis to determine the optimal placement of supports like spring hangers and anchors. This ensures that loads are distributed evenly, reducing maintenance costs and preventing unplanned shutdowns.

Balancing Flexibility and Rigidity

Piping must be flexible enough to move under stress but rigid enough to withstand wind, seismic activity, and vibration. After the 2011 Fukushima earthquake in Japan, utilities such as Tokyo Electric Power Company (TEPCO) invested heavily in advanced stress analysis for nuclear plant piping to ensure seismic resilience. This balance between flexibility and rigidity is critical in earthquake-prone regions.

Protecting Connected Equipment

Piping systems often terminate at sensitive equipment such as pumps, compressors, or reactors. If the pipe loads exceed equipment design limits, nozzles can crack or equipment can fail prematurely. Shell, in its deepwater oil projects, uses stress analysis to minimize nozzle loads on subsea equipment. This ensures reliability in harsh offshore environments where equipment replacement is extremely costly and time-consuming.

Reducing Costs and Downtime

Every hour of unplanned downtime can cost millions in industries like petrochemicals and LNG. Stress analysis helps companies like Saudi Aramco optimize their piping layouts early in design, avoiding expensive retrofits later. By preventing mid-project changes or emergency shutdowns, they save significantly on operating costs and improve overall plant uptime.

How Stress Tools Deliver These Results

Modern software such as CAESAR II, AutoPIPE, and ROHR2 follows a standard workflow:

Data Gathering – Define geometry, materials, fluids, and operating conditions.

Modeling – Create a digital representation of the piping system.

Load Cases – Simulate sustained, thermal, and occasional loads (like wind or seismic).

Analysis – Calculate stresses, forces, and displacements, comparing results to code limits.

Optimization – Adjust layout, supports, or flexibility until compliance is achieved.

Documentation – Generate reports proving system safety and code compliance.

Piping failures are not just technical issues—they can become billion-dollar disasters. By adopting stress analysis tools, companies like Chevron, ExxonMobil, GE, Shell, and Aramco have learned (sometimes the hard way) that rigorous analysis pays off in safety, compliance, and long-term savings.

In short, pipe stress analysis is not optional—it’s essential.